Case Study (Global Macro): Short Gold - 23 Apr 2024 to 3 May 2024

1. Macro Environment Background

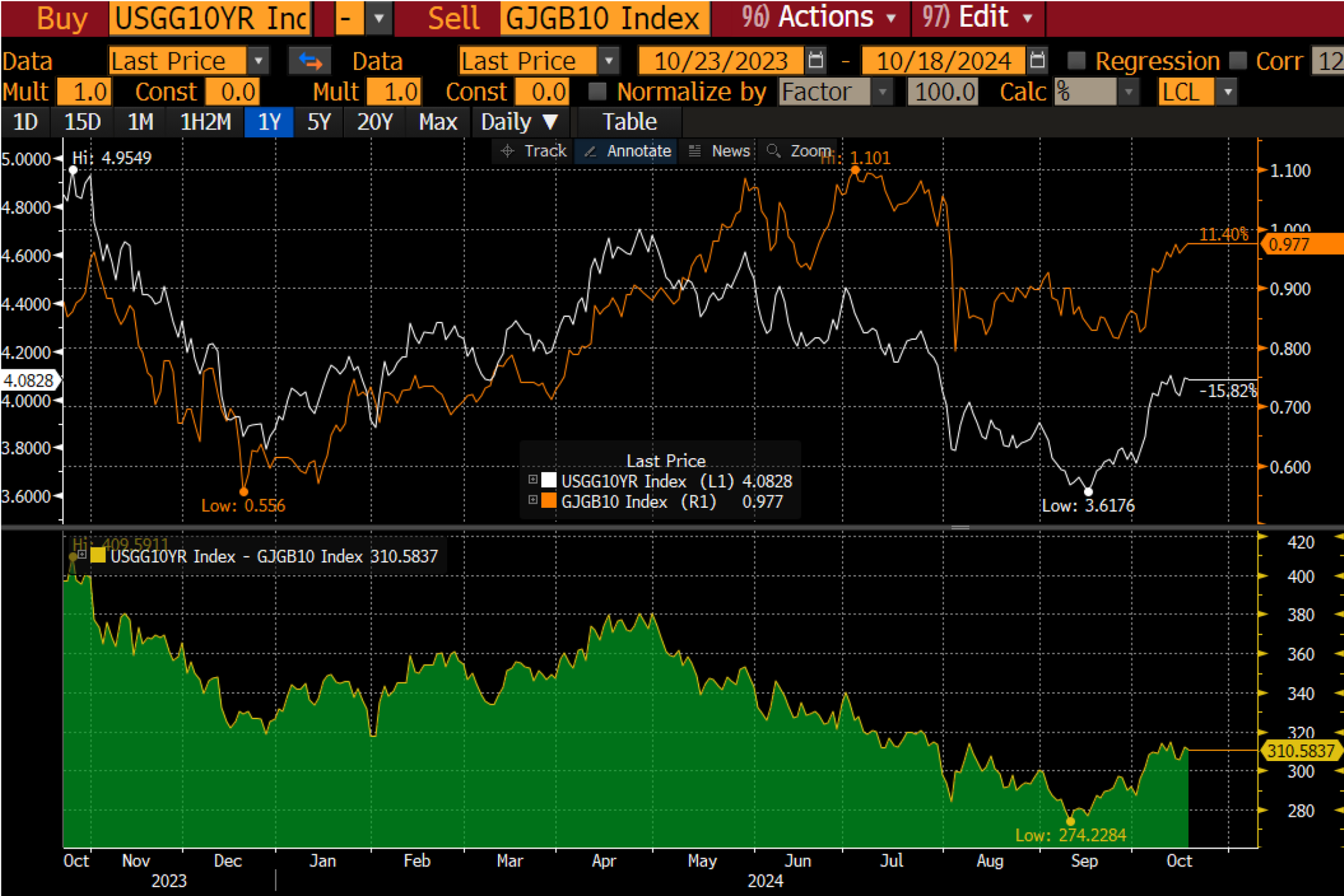

In response to inflation, global central banks raised interest rates in 2022, except for the Bank of Japan (BoJ), which maintained negative rates.

This rate differential fuelled carry trades, with investors using the low-yielding Yen to fund investments in higher-yielding assets like US equities, Gold, and Bitcoin.

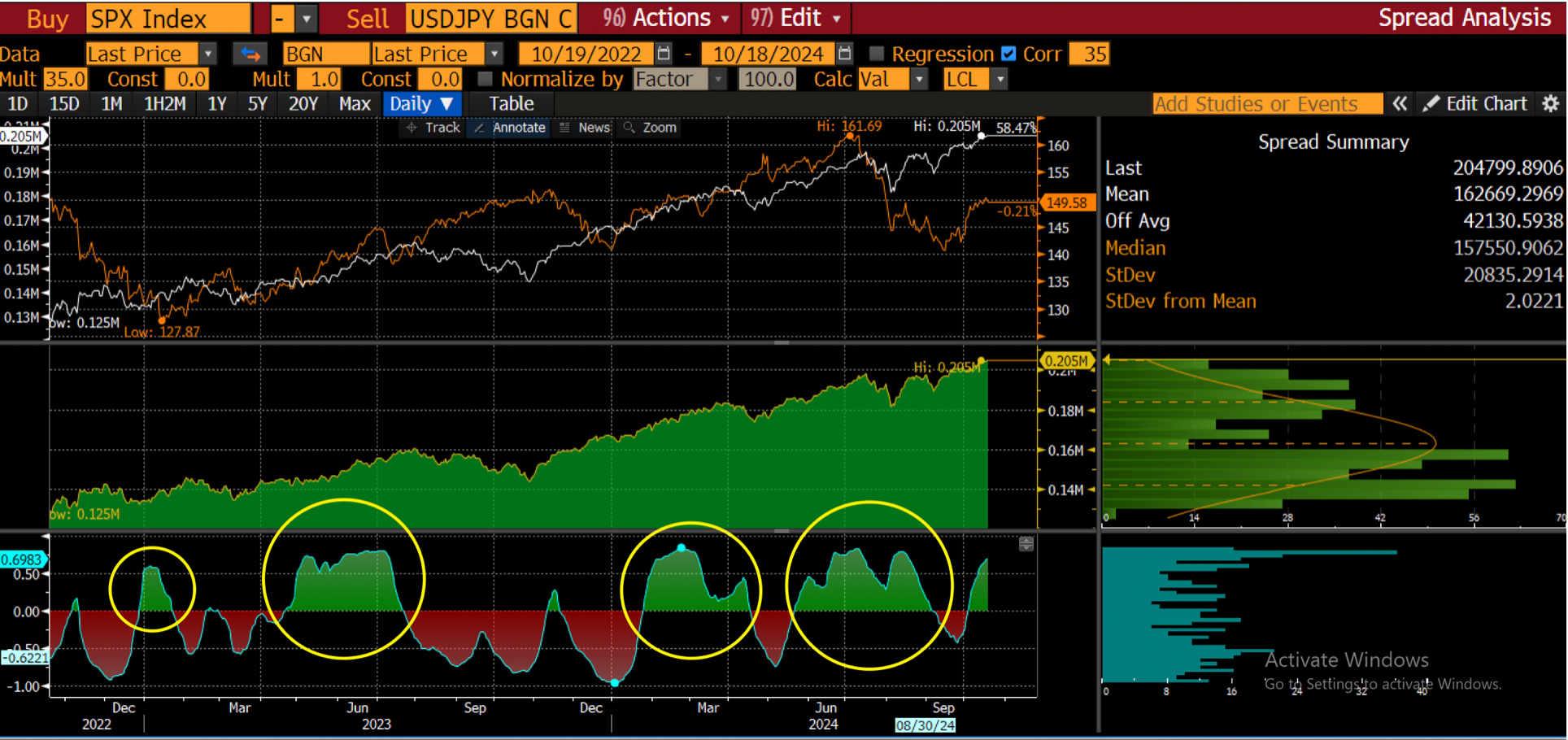

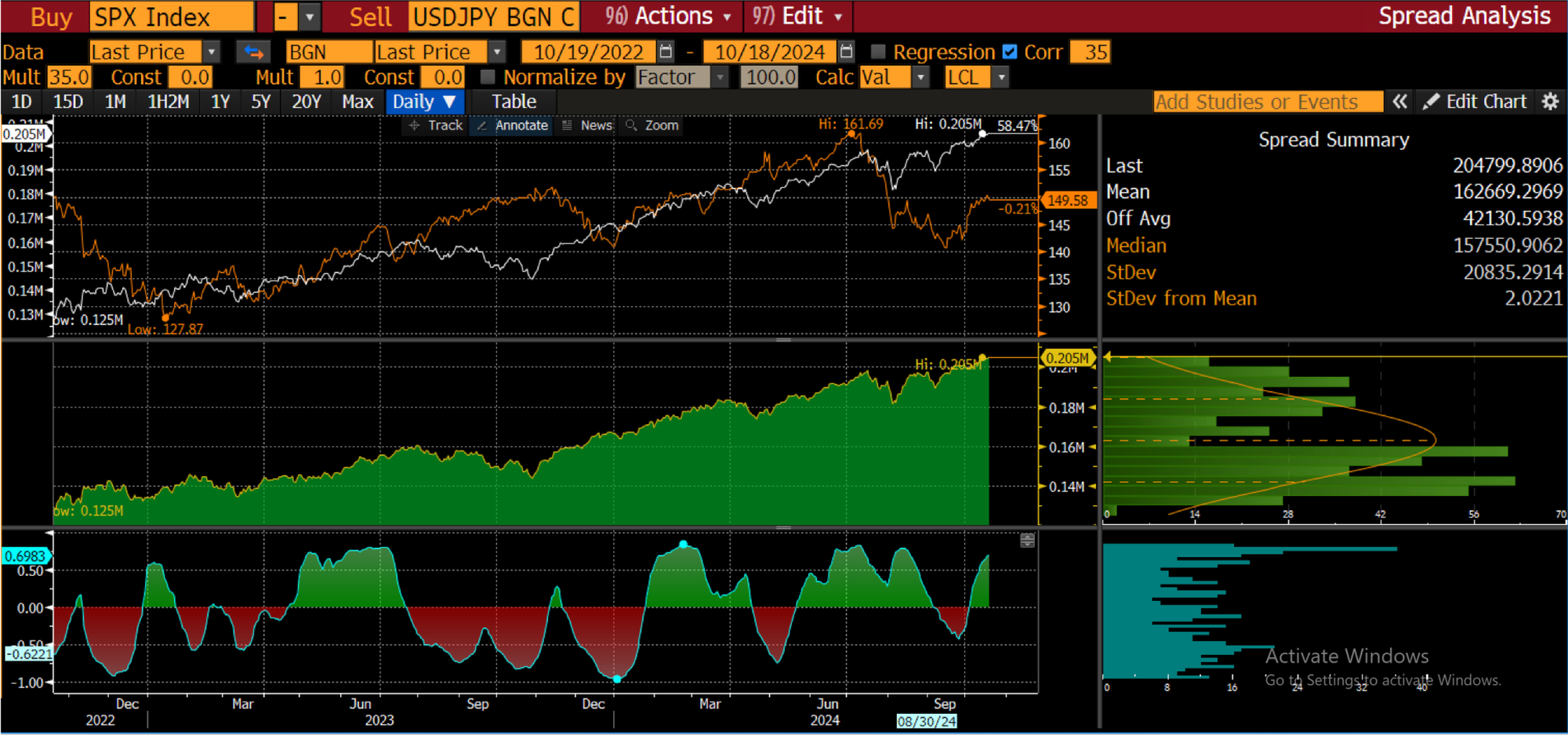

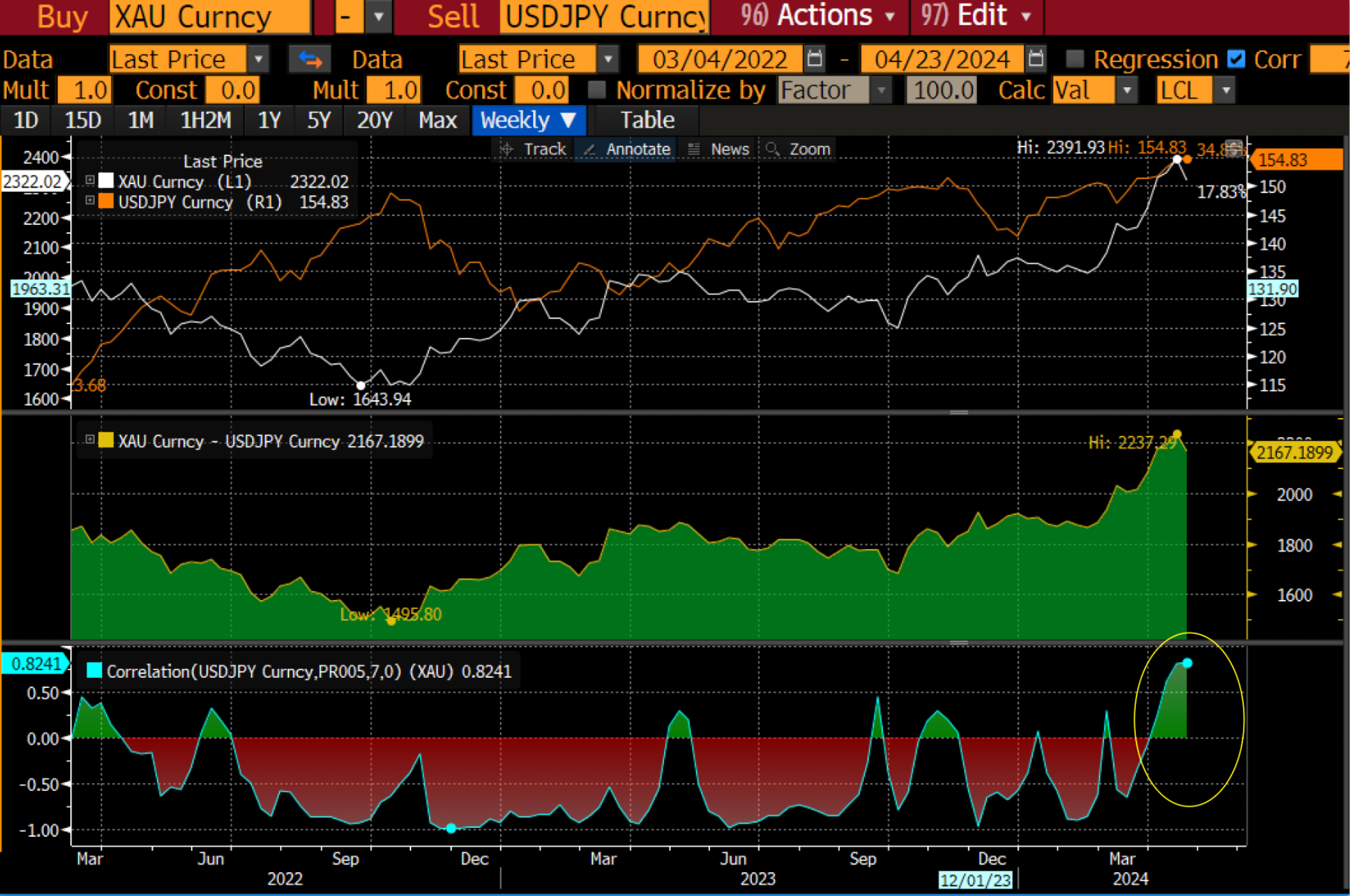

Since mid-2023, we've observed periods where USD/JPY, US yields, US equities, and Gold exhibited a positive correlation, deviating from their typical negative correlation.

2. Scenario Analysis

The positive correlation in US equities and Gold suggests a buildup in carry trades, which could unwind and negatively impact these assets under the right conditions.

Based on our research, we analysed the historical correlations between USD/JPY, yields, stocks, and gold during past carry trade unwinding events.

Rising expectations that the BoJ will end its easing policy, coupled with the Fed’s anticipated rate cuts could reverse rate differentials, potentially triggering further carry unwinding and offer correlation trade opportunity in S&P 500 & Gold.

3. Strategy Selection

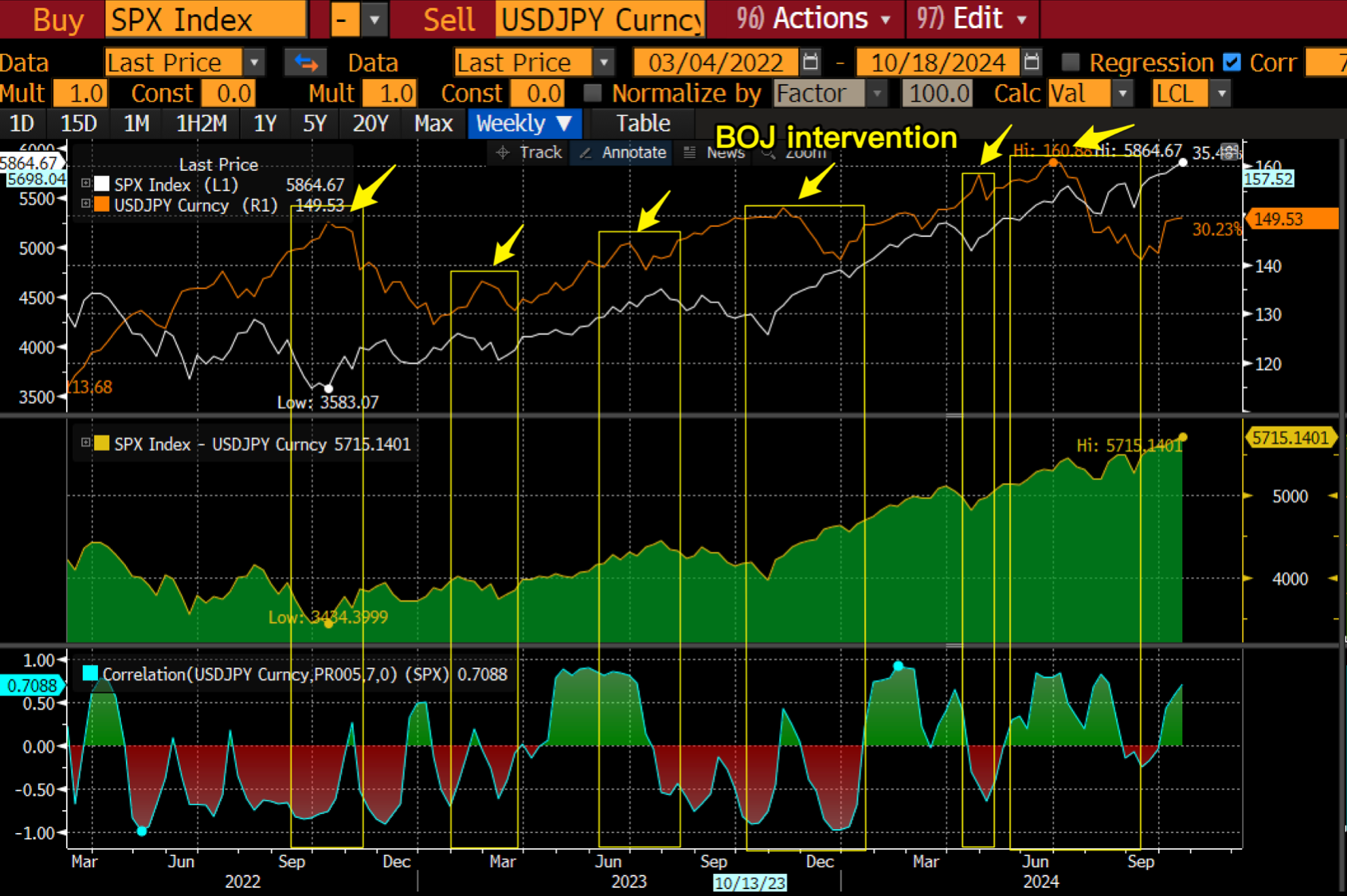

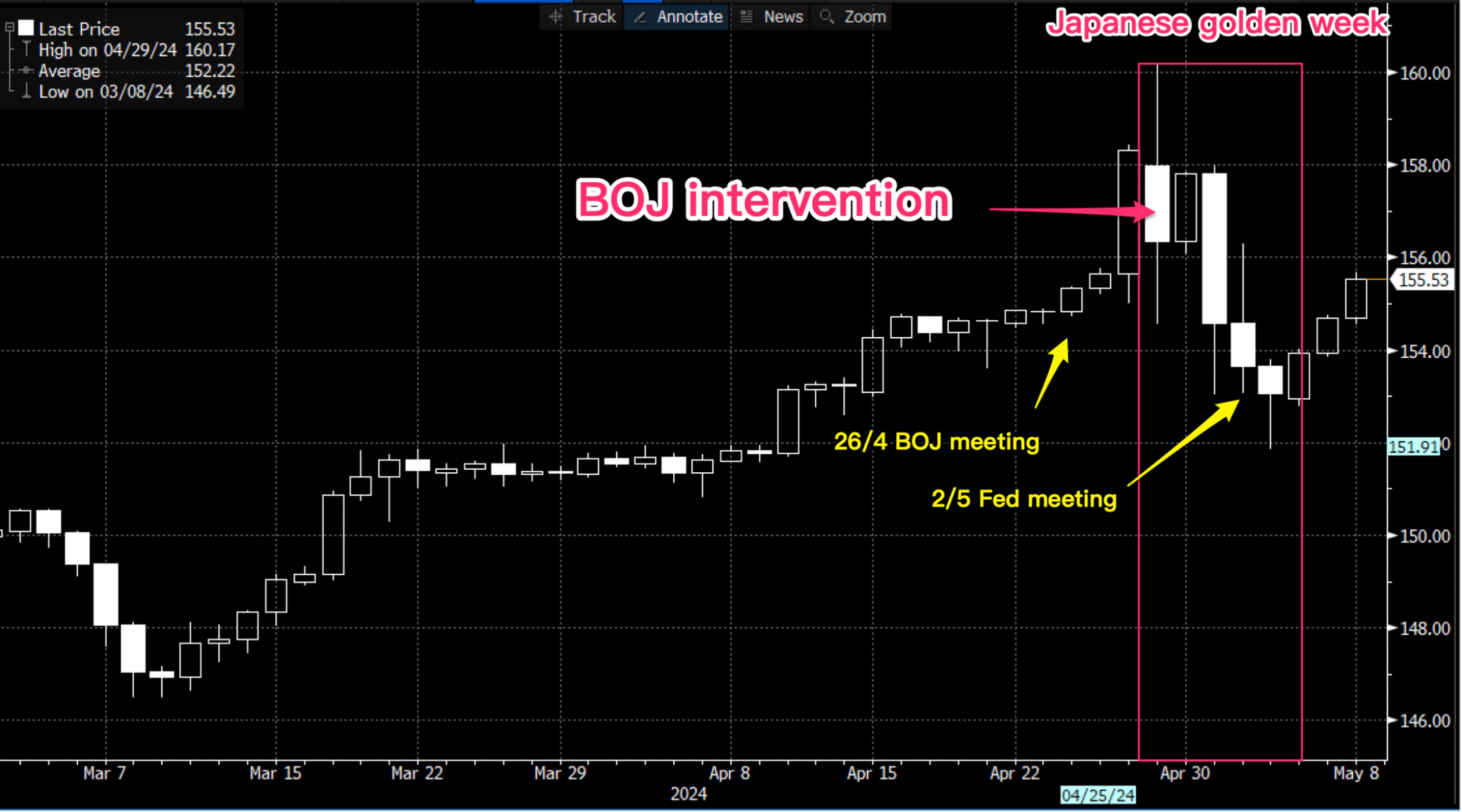

Since mid-March 2024, USD/JPY broke the critical 150 yen level, quickly approaching 160, with a positive correlation observed during this period. Meanwhile, Japanese policymakers voiced growing concerns over the Yen's depreciation, escalating intervention rhetoric.

Despite this, market participants continued selling the Yen, testing the limits of intervention, which we assessed could trigger potential intervention and a carry trade unwind.

Our strategy framework for Yen carry trades indicated the strong likelihood of impending action by the BoJ:

Yield spread consideration: Rising BOJ rate hike expectations coincides with Fed toward dovish.

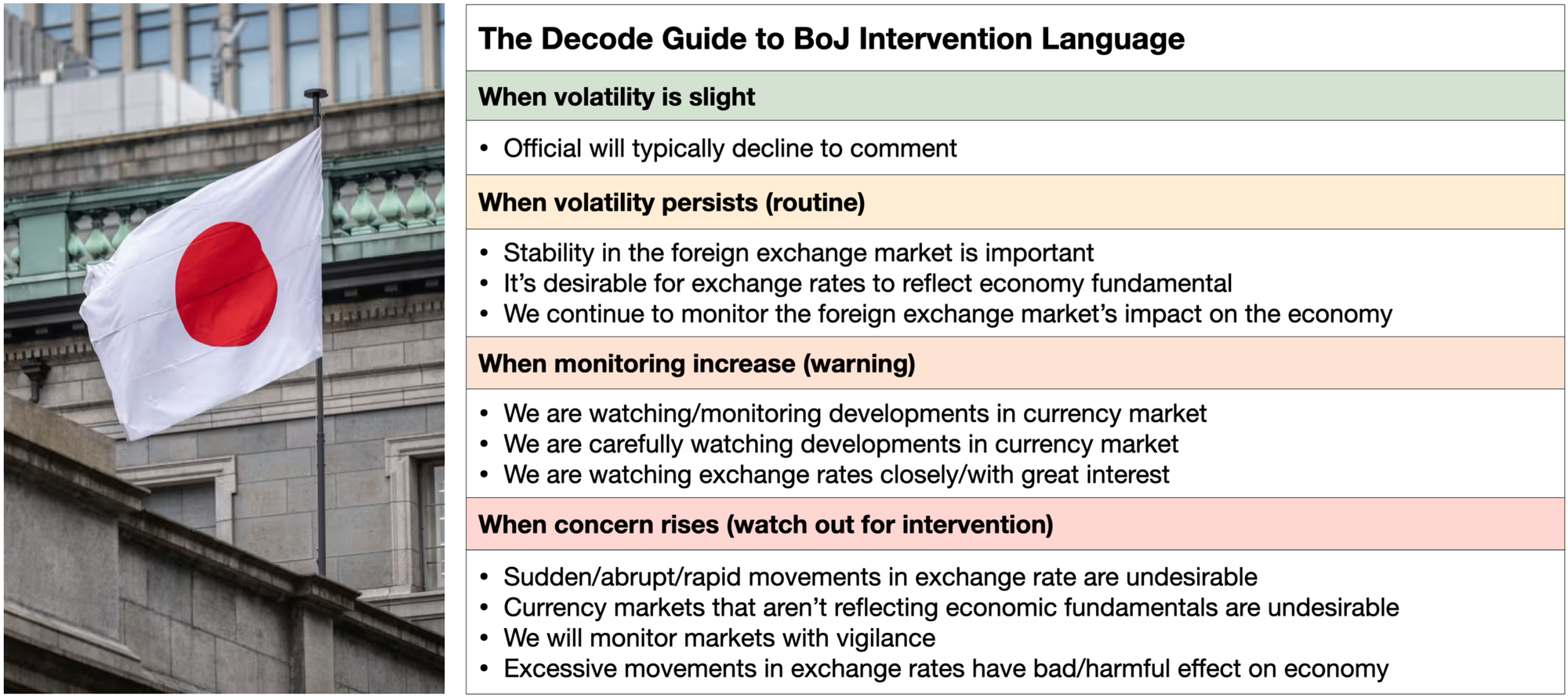

BOJ language on intervention: At the “concern rises level”

Intervention window for maximum effect: Three significant scheduled events towards the end of Apr ‘24:

- 26/4: BoJ meeting

- 2/5: Fed meeting

- 29/4 to 5/5: Japanese Golden Week

Narrative Risk: Low

4. Asset Class Selection

We decided to express our view on a possible BOJ intervention by shorting gold, based on insights from the correlation analysis and…

Additional factors in this asset class:

- Gold Purchases by Chinese Investors: In 2024, there has been a significant surge in Chinese demand for physical gold and Gold ETFs, driven by government policies aimed at creating a wealth effect amid economic challenges and low consumer confidence.

- Government Strategy: The Chinese government has increased gold purchases from foreign reserves, converting public savings into government assets. This reduces reliance on the US dollar and stimulates domestic spending.

- Impact on Prices: Rising demand has driven gold prices higher, boosting the wealth effect and further increasing domestic demand.

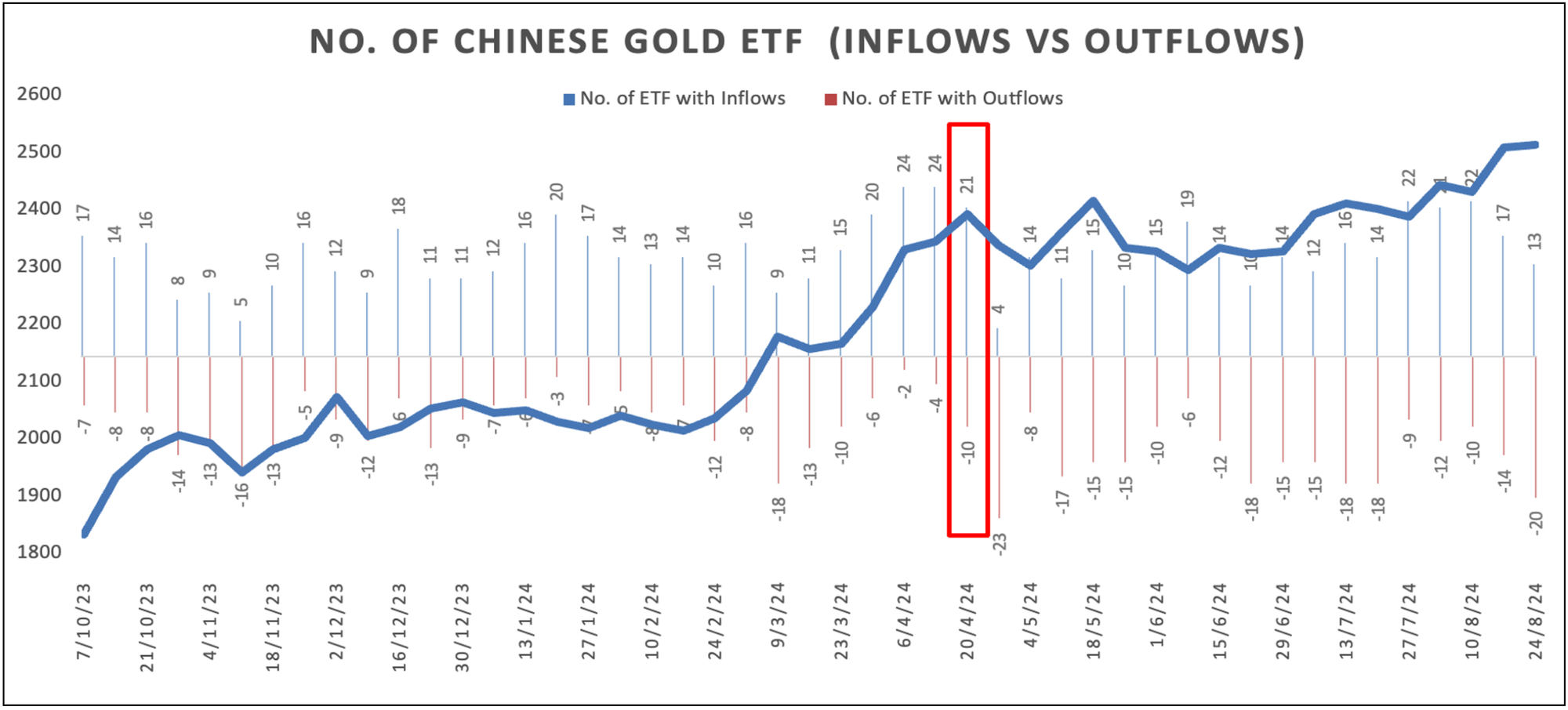

Our research showed the March 2024 gold rally was fuelled by Chinese Gold ETF inflows, while Western ETFs saw outflows. By April 20, 2024, inflows had started declining from 24 to 21, signalling potential selling pressure as Chinese buying momentum peaked.

Gold spiked above $2,400 but quickly retreated. Sentiment indicators showed signs of exhaustion, pulling back from overbought levels.

Position Risk: Low

5. Execution and Ongoing Monitoring

We saw this as an opportune time to short Gold, supported by low-risk ratings for both BoJ intervention narratives and gold positioning, along with key indicators:

- The upcoming week provided an ideal window for BoJ intervention, which could trigger a carry unwind and negatively impact gold.

- Yen positioning was at historical lows, with technical indicators suggesting prices were significantly overstretched.

- By the week of April 20, 2024, Gold ETF inflows had declined from historical highs, dropping from 24 to 21.

Entry point:

- 2024-04-23: Short Gold 2,318.227

Exit point:

- 2024-05-03: Exited 2,284.50