Q1 2025 Quarterly Report

Review: Focused Market Narratives Guiding Our Q1 Strategy

The first quarter of 2025 presented a dynamic and rapidly evolving market environment, shaped by shifting macroeconomic conditions, trade policy developments, and investor sentiment adjustments.

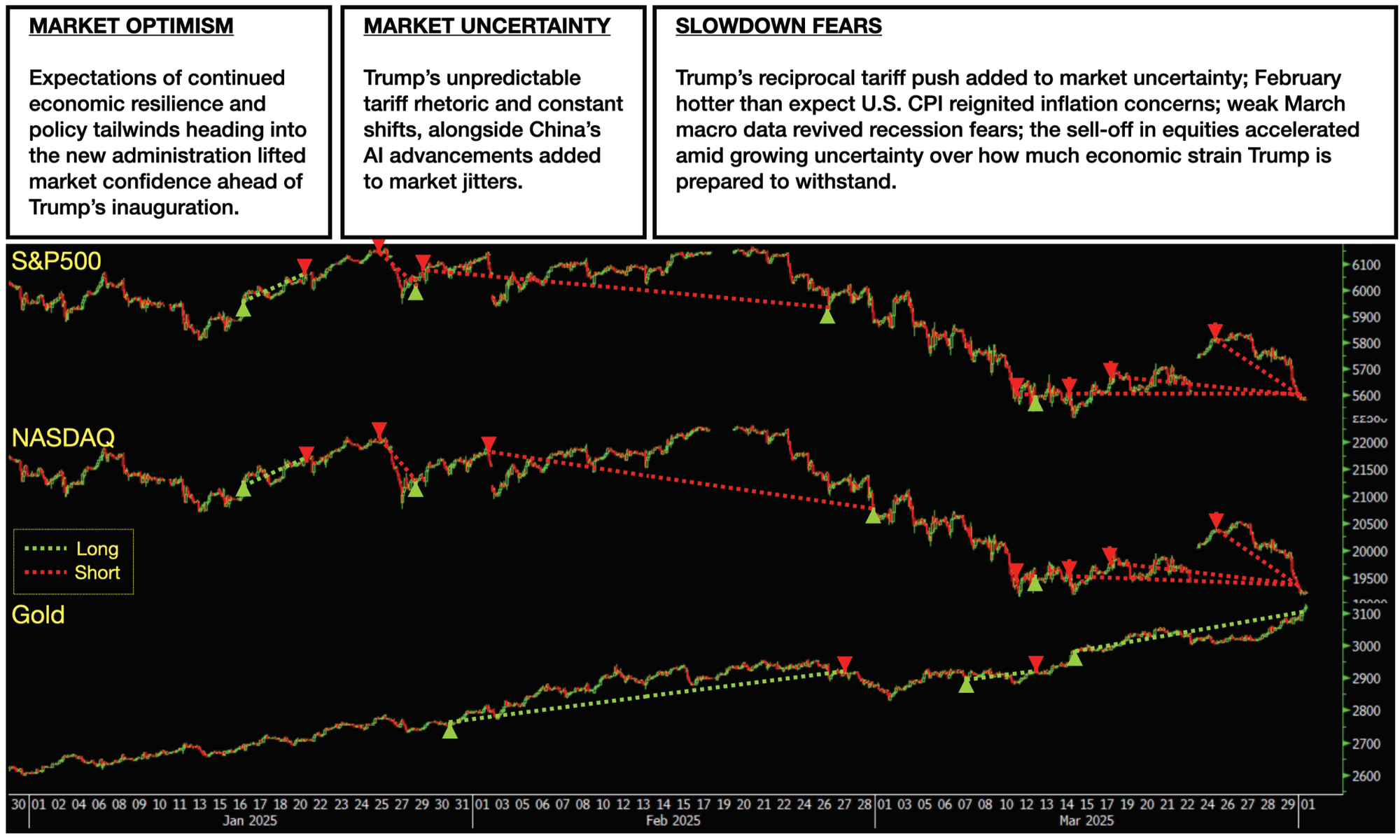

The year began with strong optimism, driven by expectations that the U.S. economy would continue to outpace its global peers. This sentiment was supported by anticipations of pro-business policies under the Trump administration, resilient U.S. economic growth data, and robust corporate earnings – particularly in the technology sector. The theme of American exceptionalism fuelled a broad-based rally in U.S. equities and the U.S Dollar, reinforcing risk-on sentiment among investors.

However, this optimism was soon tempered as President Trump reignited trade war rhetoric and introduced new tariffs following his inauguration, rekindling concerns over global growth and inflation. Market volatility increased as investors began pricing in the risks of slower earnings growth and rising input costs, leading to a more cautious reassessment of equity valuations.

At the same time, the announcement of China’s Deepseek raised concerns over the competitive valuation and market share of American tech firms. This development added to market jitters and weighed on high-growth names that had previously led market gains.

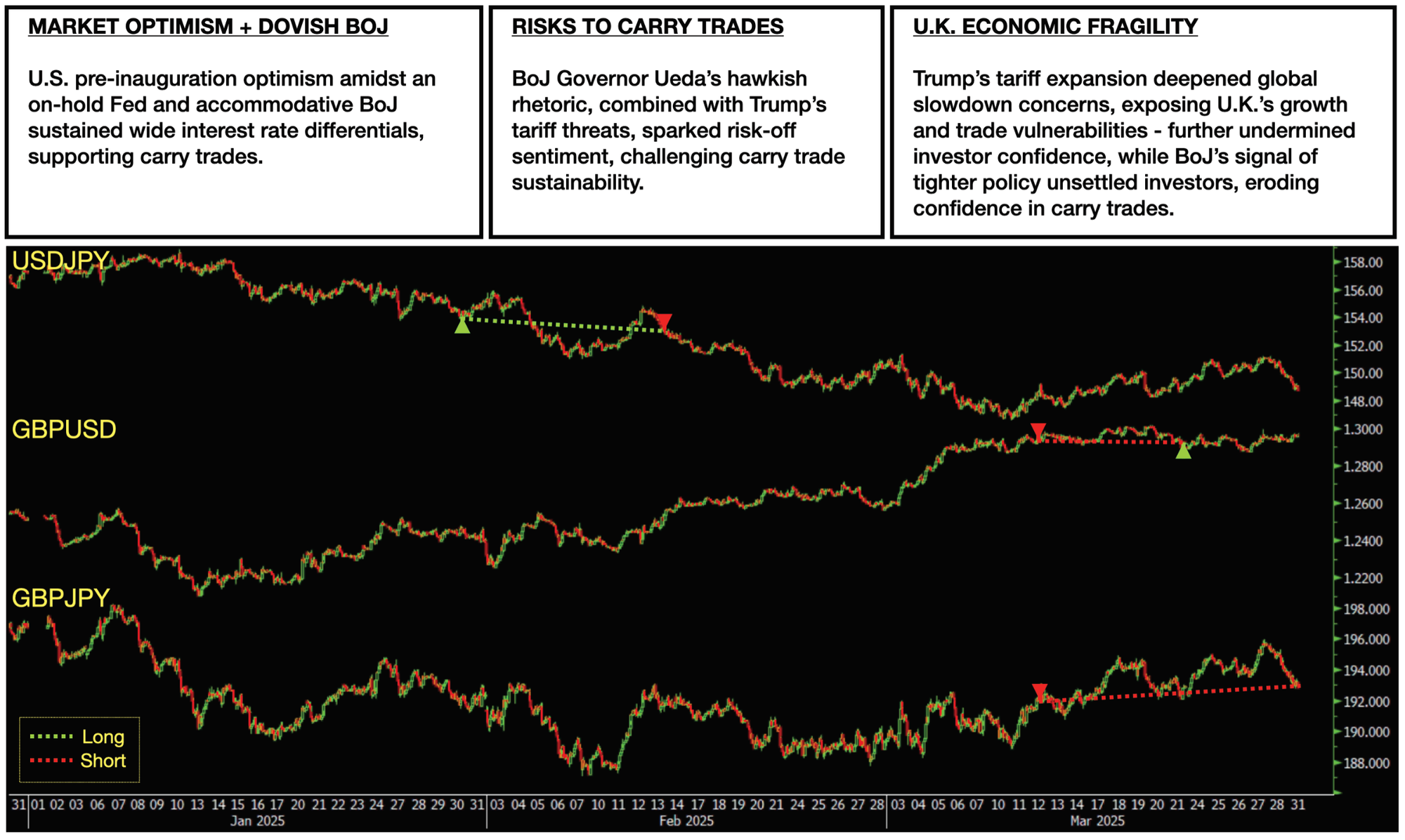

Currency markets also reflected these developments – early strength in the U.S. Dollar, underpinned by elevated U.S. Treasury yields supported carry trade flows into pairs like USD/JPY as the Yen remained weak supported by the Bank of Japan’s (“BoJ”) continued dovish stance in addition to rising retail short Yen positions. However, the first BoJ meeting of 2025 marked a change – Governor Ueda’s increasingly hawkish rhetoric on the back of strengthening Japanese economic data amid a risk-off environment strengthened the Yen outlook and signaled challenges to carry trade flows.

Meanwhile, the U.K. economy encountered weakening domestic demand as consumers and businesses grew cautious, driven by a mix of economic and political uncertainty, reducing spending and investment. The government also pursued fiscal restraint, tightening budgets to stabilise public finances, which further limited growth. Additionally, vulnerabilities emerged from U.S. trade tensions, risking disruption to export markets and exposing the economy to broader global pressures.

By mid-quarter, the release of a high U.S. CPI reading surprised markets, reigniting fears that inflation could remain persistent. Also, U.S. Retail Sales faced the sharpest decline in two years alongside weakening momentum in a broad range of economic indicators including the labour market, stoking recessionary fears. Furthermore, the “Trump put” was nowhere in sight when President Trump did not provide any affirmation to Wall Street who wondered how much pain he will have the U.S. economy endure. Although U.S equities staged a brief rebound upon entering correction territory later in the quarter, a constantly shifting President Trump caused markets to remain uncertain.

Adding to the overall uncertainty, President Trump's sweeping assertion of executive power since returning to the White House has tested the limits of the domestic constitutional system and raised concerns over broader disruptions to the global order. These actions have amplified fears of policy instability and increased the prospect of geopolitical and economic spillovers.

As a result, a heightened sense of unpredictability prevailed, reinforcing the bearish tone that persisted through the end of Q1.

From Narrative to Strategy: Q1 Trades Positioning

The risk-on sentiment at the beginning of the quarter, as supported by continued economic resilience and policy tailwinds heading into the new administration, provided us with a low risk rating to initiate long positions in U.S. equities based upon a Global Macro strategy. However, initial optimism leading up to President Trump’s inauguration were challenged as market participants awaited concrete policy announcements while stretched technical and sentiment indicators in U.S. equities indicated a potential mispricing scenario.

President Trump’s unpredictable trade rhetoric shifted markets toward a volatile and risk-off environment, as investors grappled with abrupt trade policy announcements. In response to this fundamental turn in market dynamics, we pivoted to a risk-off approach under a Global Macro strategy, shorting U.S. equities to capitalize on sustained policy and geopolitical uncertainty.

Alongside our shift to a risk-off stance in U.S. equities, in-line with our initial outlook, we recognized a low-risk opportunity to adopt a Global Macro strategy in Gold, initiating long positions to capture safe-haven flows. Furthermore, Gold’s enduring role as a store of value during periods of macroeconomic dislocation reasserted itself as a clear beneficiary, appealing to both investors seeking to hedge their high-valuation equity exposure and those reallocating away from their core equity holdings.

Additionally, the asset benefited from structural tailwinds, including record central bank purchases and policy shifts in China that allowed domestic insurers to allocate to Gold, adding another layer of support, potentially unlocking fresh investment flows. In addition, market participants are still expecting the Fed to lower borrowing costs this year, as lower yields support non-interest-bearing assets like Gold.

As for our carry and currency trades, January’s risk-on sentiment and the BoJ’s accommodative stance supported Yen weakness, offering a medium-risk opportunity for us to establish a carry trade position to long USD/JPY within our Carry Trade strategy. However, prevailing risk-off sentiment and hawkish BoJ rhetoric signaled challenges to carry trades, prompting us to close the position and monitor the evolving dynamics.

Progressing into late Q1, the Yen attracted safe-haven demand amid an escalating global trade war, bolstered further by narrowing interest rate differentials with major economies – acting as a tailwind for the traditionally low-yielding Yen and limiting its downside.

Concurrently, against a fragile U.K. backdrop, we initiated short positions in GBP/USD and GBP/JPY within our Global Macro and Carry Trade strategies to express our expectation that the Pound will weaken against the U.S. Dollar amid a firming Yen. However, as market sentiment became increasingly unclear and GBP/USD fell into range-bound fluctuation with no clear direction, we decided to close the GBP/USD position and reassess the unfolding developments.

Open Positions Heading Into Q2

We view current conditions as reflective of a broad risk-off environment. Going into Q2, we maintain short on S&P500, NASDAQ, long Gold, as well as short GBP/JPY.

Outlook: Focused Market Narratives Guiding Our Q2 Strategy

As the uncertainty from President Trump’s confrontational policy style continues, we expect U.S. equities to remain pressured – market participants will likely focus on the intensity and the pace of policy implementation by the U.S. administration, particularly tariffs, and the economic and geopolitical responses that could strain global economies.

Without signs of easing, the ongoing trade tension may heighten U.S. growth concerns. Globally, a prolonged standoff risks deepening American isolationism, especially as Europe and China seize shifting economic opportunities. Europe, strengthened by German and EU-wide fiscal moves toward unified defense spending, could enhance integration and attract capital escaping U.S. volatility.

Domestically, unrelenting trade war rhetoric and the potential implementation of tariffs could squeeze U.S. economic vitality, shrinking corporate profit margins and deterring long-term investment. As tariffs drive up import costs they could sustain elevated inflation, potentially prompting tighter monetary policy and higher borrowing costs – weighing on consumer spending, hinder business growth, and intensify slowdown fears, all of which could further cloud the outlook for U.S. economic resilience.

Against this backdrop, we maintain our bearish view on U.S. equities, as escalating trade rhetoric and growing market uncertainty continue to overshadow the recent rebound. The market’s next move, whether it is a new round of sell-off or a tentative calm, depends on the evolution of Trump’s policy, as well as the guidance of economic data. We will zero in on the intensity of Trump’s tariff policies and center around underlying growth momentum as key drivers. Should tariff-driven pressures lead to renewed economic slowdown fears alongside rising inflation data, stagflationary concerns might be rekindled resulting in downside risks for equities – while cooler prints might offer brief respites, our bearish stance remains. First quarter corporate earnings will also shape sentiment, possibly revealing cracks in technology and industrial sectors burdened by tariff costs. This data-driven environment underscores economic releases as the main force behind U.S. equity swings, likely prolonging volatility through Q2 absent a game-changing shift.

Furthermore, since mid-March, a weaker U.S. Dollar policy push from Council of Economic Advisers (“CEA”) Chairman Stephen Miran, could weaken America's ability to influence global markets, attract capital, and maintain dominance through its currency and asset appeal. This is likely to trigger investors to reassess the stability that once underpinned the appeal of U.S. equities – spurring portfolio reallocation away from overvalued U.S. assets to more attractive markets like Europe and China, alongside safe-haven assets including Gold, Yen and Euro.

Gold, the top performing asset so far this year, is poised to remain supported as a premier safe-haven amid persistent U.S. trade war uncertainty, tariff-driven inflation, and a potential U.S. economic slowdown. The Yen, bolstered by Japan’s economic resilience and the BoJ Governor Ueda’s hawkish stance, is set for appreciation with expectations for additional rate hikes on the horizon, reinforcing its safe-haven appeal and challenging Yen carry trades as yield gaps with the U.S. narrow.

We note that a prolonged reallocation to safe-haven assets would involve unwinding hedges and a gradual transition, whereas short-term movements may see funds temporarily parked in defensive assets when risk-off sentiment intensifies – such moves are susceptible to fall when market goes risk-on again. Thus it is crucial to use the right lens to assess the type of flows that are occurring given the prevailing fundamental developments. Though markets are continually adjusting to President Trump’s tactics, uncertainty lingers over their scope and economic impact.

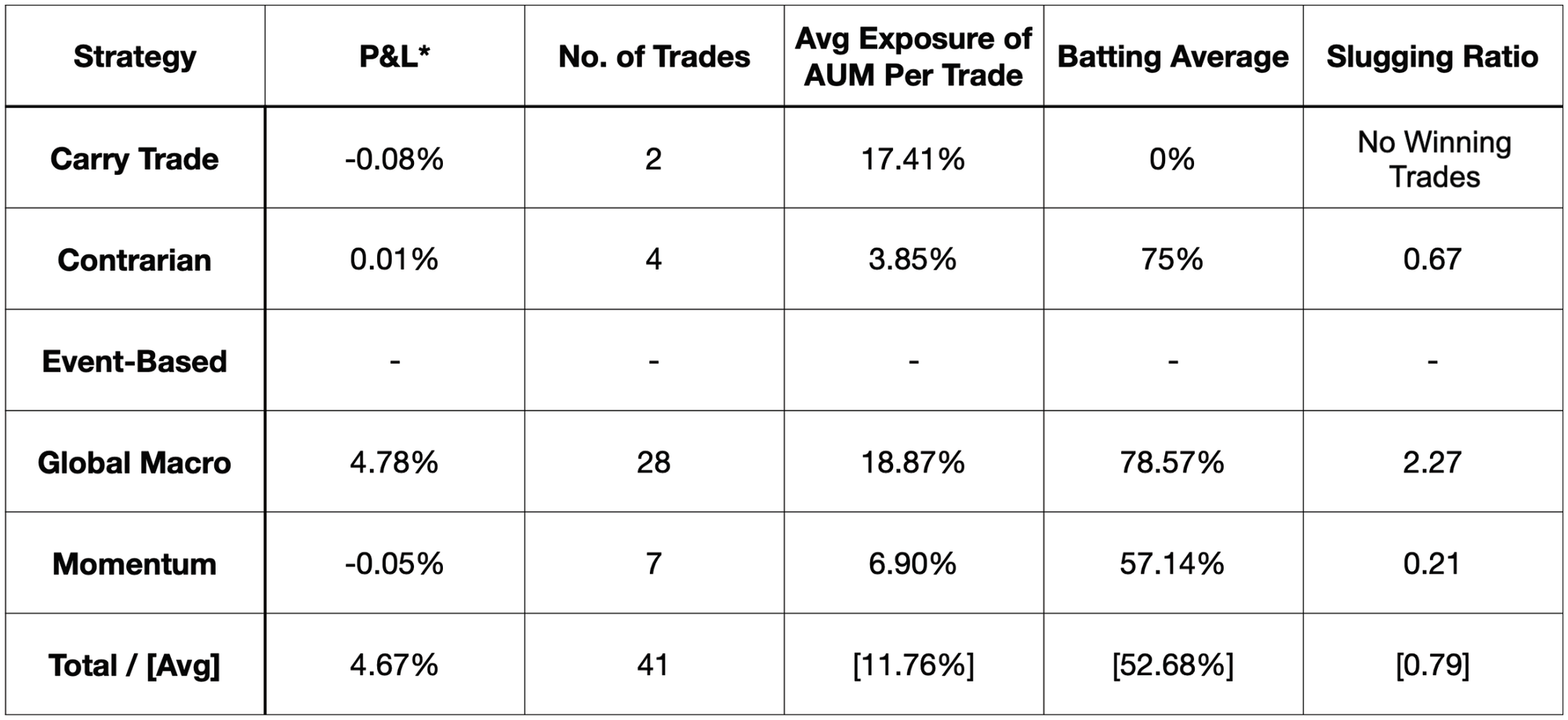

Q1 2025 Trades Attribution by Strategy

As we navigate an increasingly complex and fluid macro environment, our focus remains on preserving capital, identifying asymmetric opportunities, and maintaining a high degree of flexibility in our strategy execution. We will continue to adapt our positioning in response to evolving market narratives while remaining grounded in our disciplined, data-driven investment process.

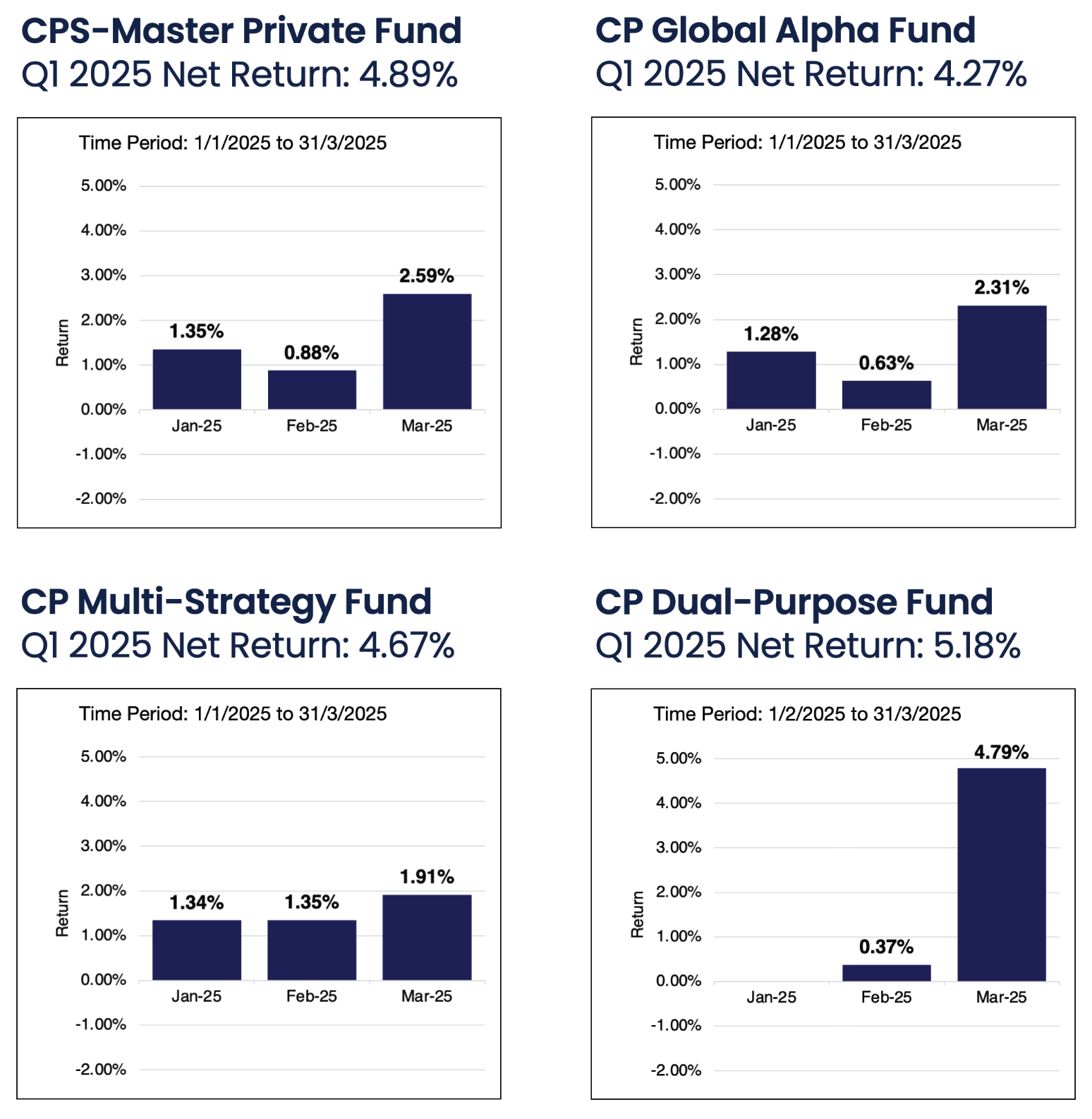

Q1 2025 Monthly Net Returns

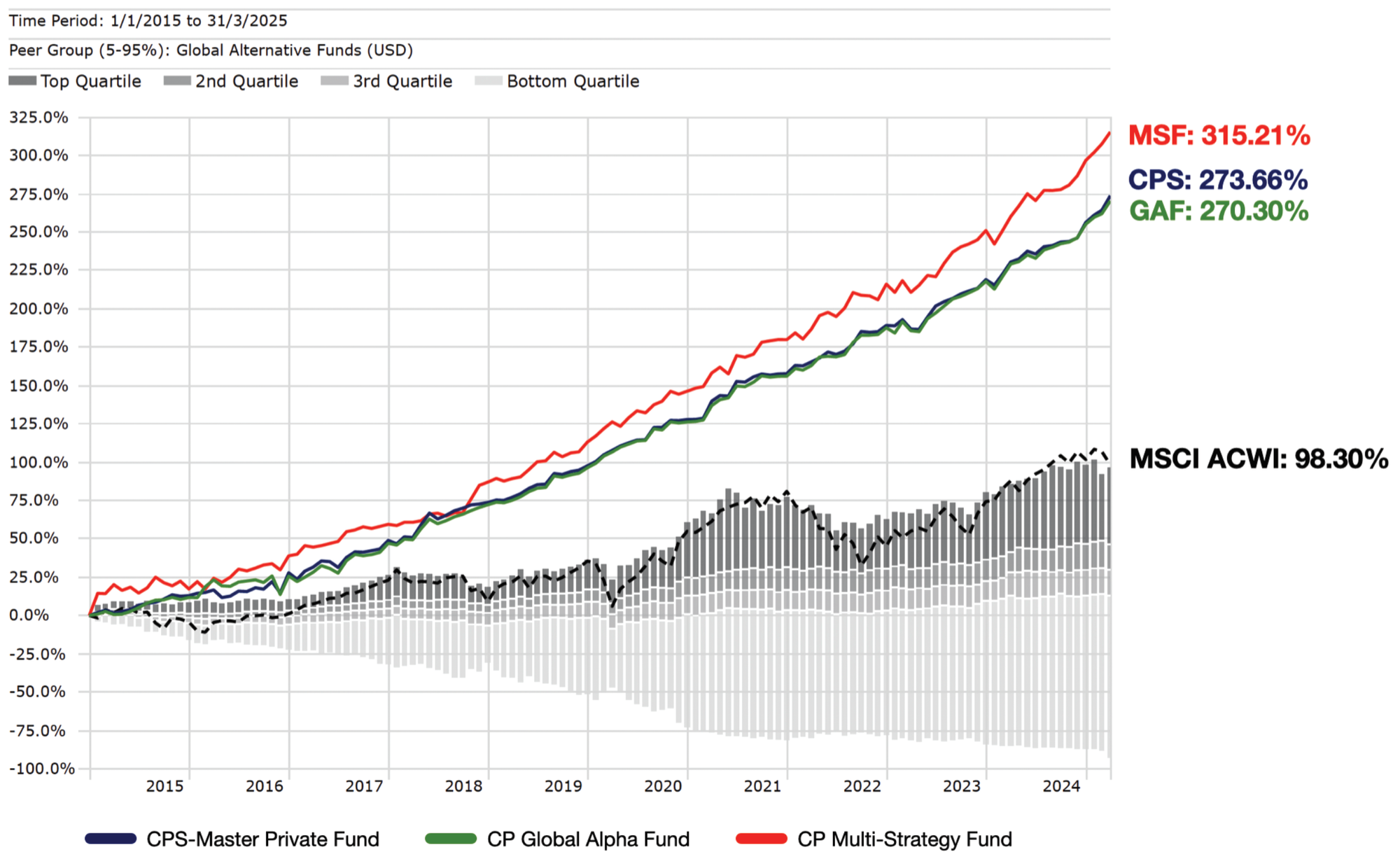

Long-Term Cumulative Performance

Disclaimer

This report has been prepared for the purpose of providing general information only without taking account of any particular investor’s objectives, financial situation or needs, and does not amount to an investment recommendation. In all cases, the information in this document does not constitute a solicitation for investment. Any offer can only be made with the relevant offering documents, together with the relevant private placement memorandum, all of which must be read and understood in their entirety, and only in jurisdictions where such an offer is in compliance with relevant laws and regulatory requirements.

You should always bear in mind that the value of investments and any income from them may go up as well as down, and past performance should not be seen as an indication of future performance.