De-dollarisation / USD Concerns

For years now, we have repeatedly addressed concerns regarding USD-denominated CP funds each time the issue of potential Dollar weakness arises. This includes periods such as during the implementation of quantitative easing (QE) and zero-interest-rate policies, or post-pandemic Modern Monetary Theory (MMT) policies. The implementation of these measures sparked concerns about an increase in the money supply, which some believe could eventually lead to a weakening of the Dollar. This has fuelled popular discussions recently about de-dollarisation, with some arguing that a decrease in demand for the Dollar could ultimately erode its value.

However, time and again, the actual outcome was the opposite, with the Dollar strengthening rather than weakening through the course of these policies. Gaining an understanding of the dynamics of financial market behaviour is essential, as quantifying the relationship between supply and demand to determine price values is not always applicable in real-world market scenarios. We would be delighted to delve further into this topic in the future.

For now, our focus is on whether investors should be concerned about USD fluctuations when investing in CP funds. To address this, we will consider both theoretical and practical perspectives, supported by historical data.

In this discussion, it's essential to acknowledge that major currencies typically move in cycles within the same economic system; which is currently dominated by democratic capitalism. To stay on topic, let us focus our discussion on the concerns of investing during periods of Dollar weakness, rather than engaging in hypothetical speculation about the potential collapse of currency if the capitalism system were to be replaced. We believe that in such an unlikely and drastic scenario, our concerns would shift away from investment topics to more fundamental matters related to our livelihoods…

Q1. I am concerned about the weakening USD; should I consider redeeming my USD-denominated assets (CP funds, other USD-denominated funds, US stocks, US properties, ETFs, trading accounts, etc.)?

When making investment decisions, the primary consideration should be the value of the asset itself, rather than the underlying settlement denomination.

You should evaluate whether the asset you've invested in is expected to deliver value or functionality, such as increasing net asset value, generating income, or providing facilities.

The secondary consideration involves exchange risk, particularly if your local currency is not the US dollar. You need to assess whether the potential value of an asset outweighs the exchange risk. Professional investors generally do not sacrifice the potential value of an asset due to exchange risks, unless the asset's potential value appears bleak. If needed, you can also hedge your currency exposure, provided the hedging cost is lower than the expected exchange risk.

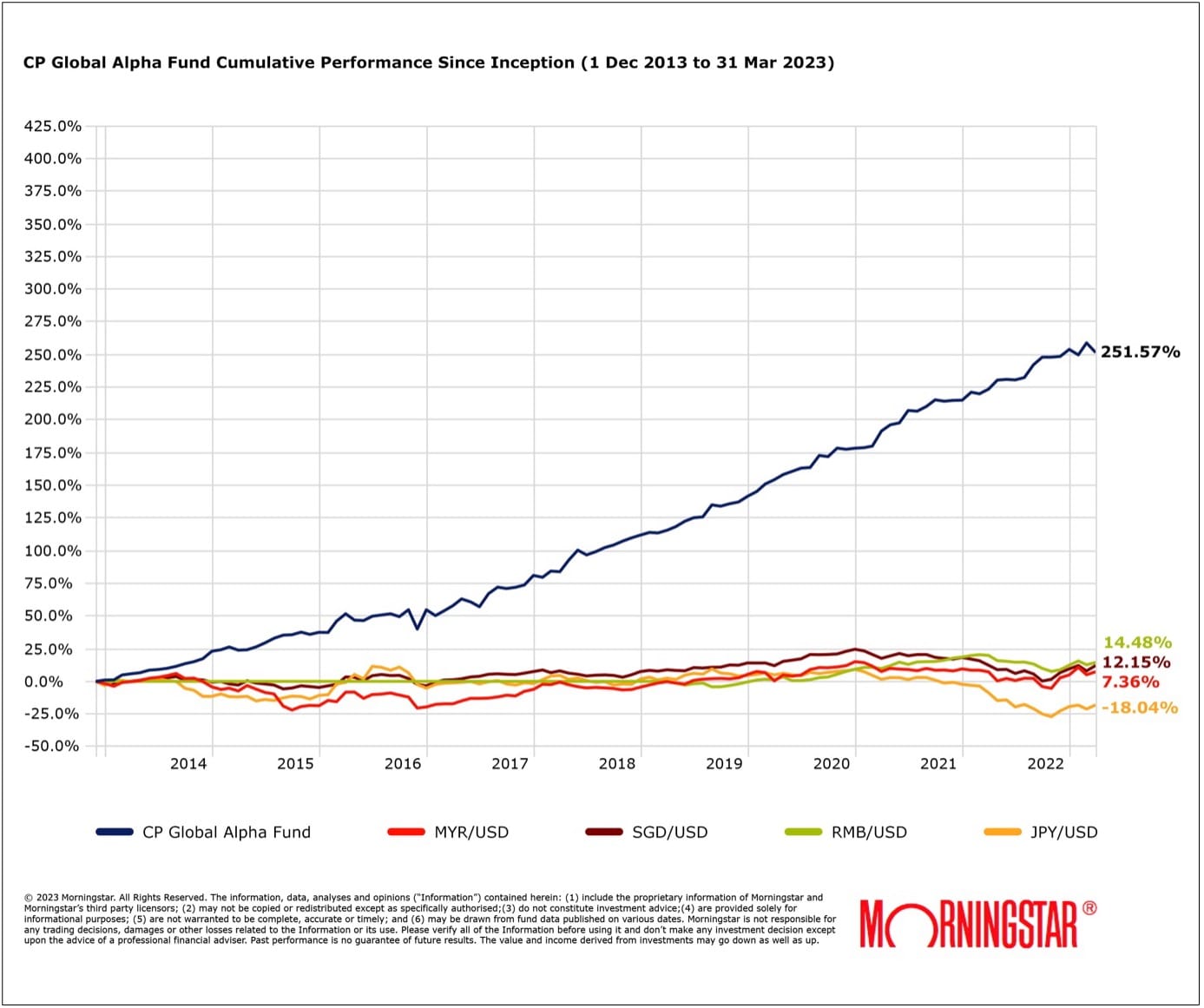

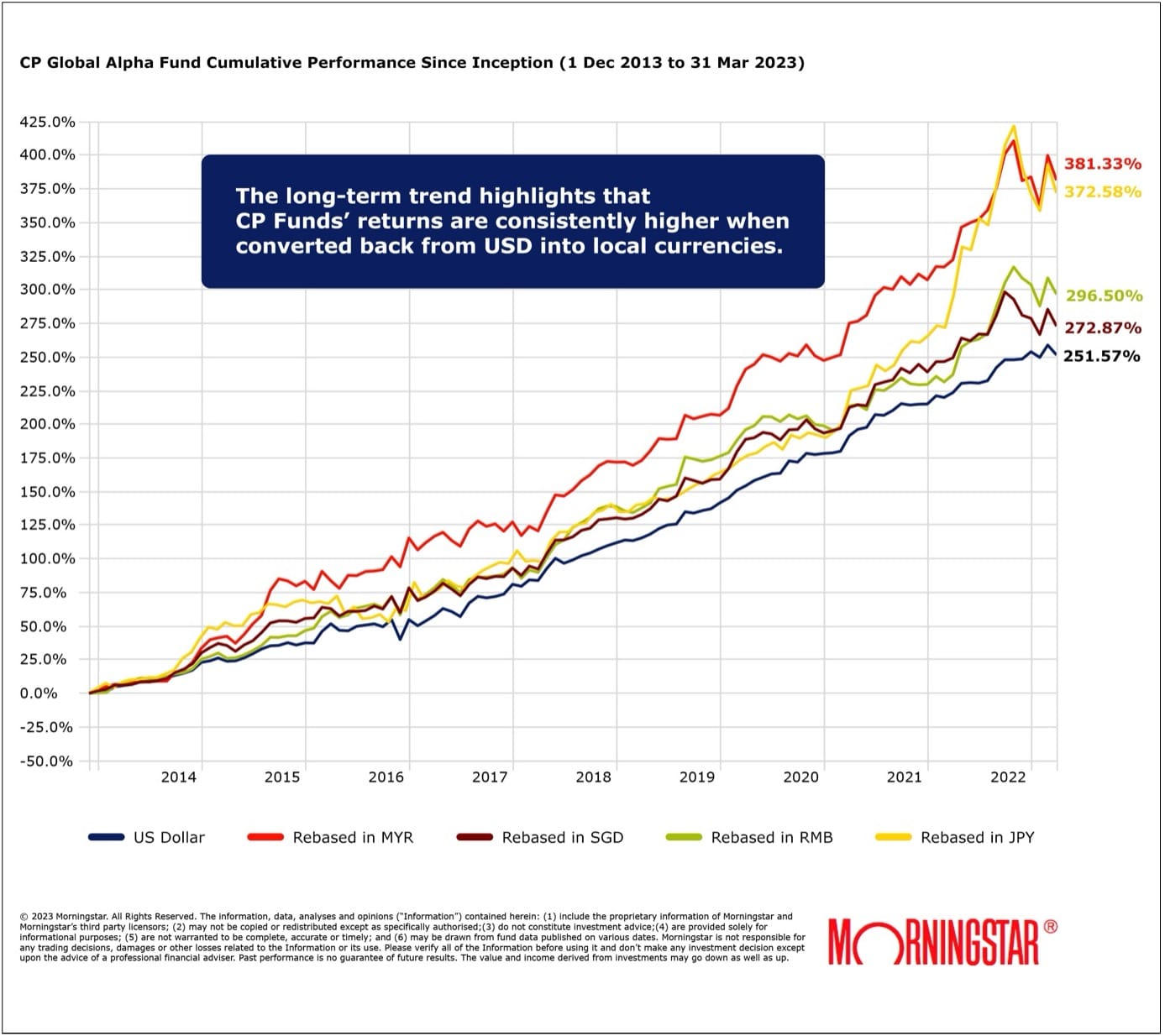

Thus, the primary concern of this question is whether the USD-denominated asset presents you with good potential value (which exceeds the exchange risk). When discussing CP funds, the answer becomes very clear, as can be seen in our long-term track record (Chart 1), time and again, the growth in value of our funds outweighs exchange risks.

Chart 1: Long-Term CP Fund Performance Against Selected Local Currencies

Q2. Which asset classes should be considered for hedging against USD depreciation?

To hedge against USD depreciation, you should consider investing in asset classes that have a negative correlation with the USD.

Theoretically, gold and oil are popular choices to hedge against the US Dollar and inflation (currency depreciation that requires more dollars to purchase the same goods). This is because gold, oil, and most commodity contracts are denominated in USD, and markets tend to price them higher to account for the depreciation of the Dollar.

Thus, using gold or oil as a hedge against the Dollar can theoretically help offset potential losses (hedging is meant to offset losses, not provide additional gains). However, numerous factors can influence asset prices, and while theoretically these assets may provide some cushion against losses, they may not be entirely effective, as demonstrated by historical statistics:

Chart 2: Performance of Gold During Dollar Weakening Cycles

Positive Example:

- During 2017: Dollar (blue line) weakened, while Gold (white line) strengthened

Negative Example:

- During 2020-2021: Dollar weakened, Gold went up but moved down after Q3 2020

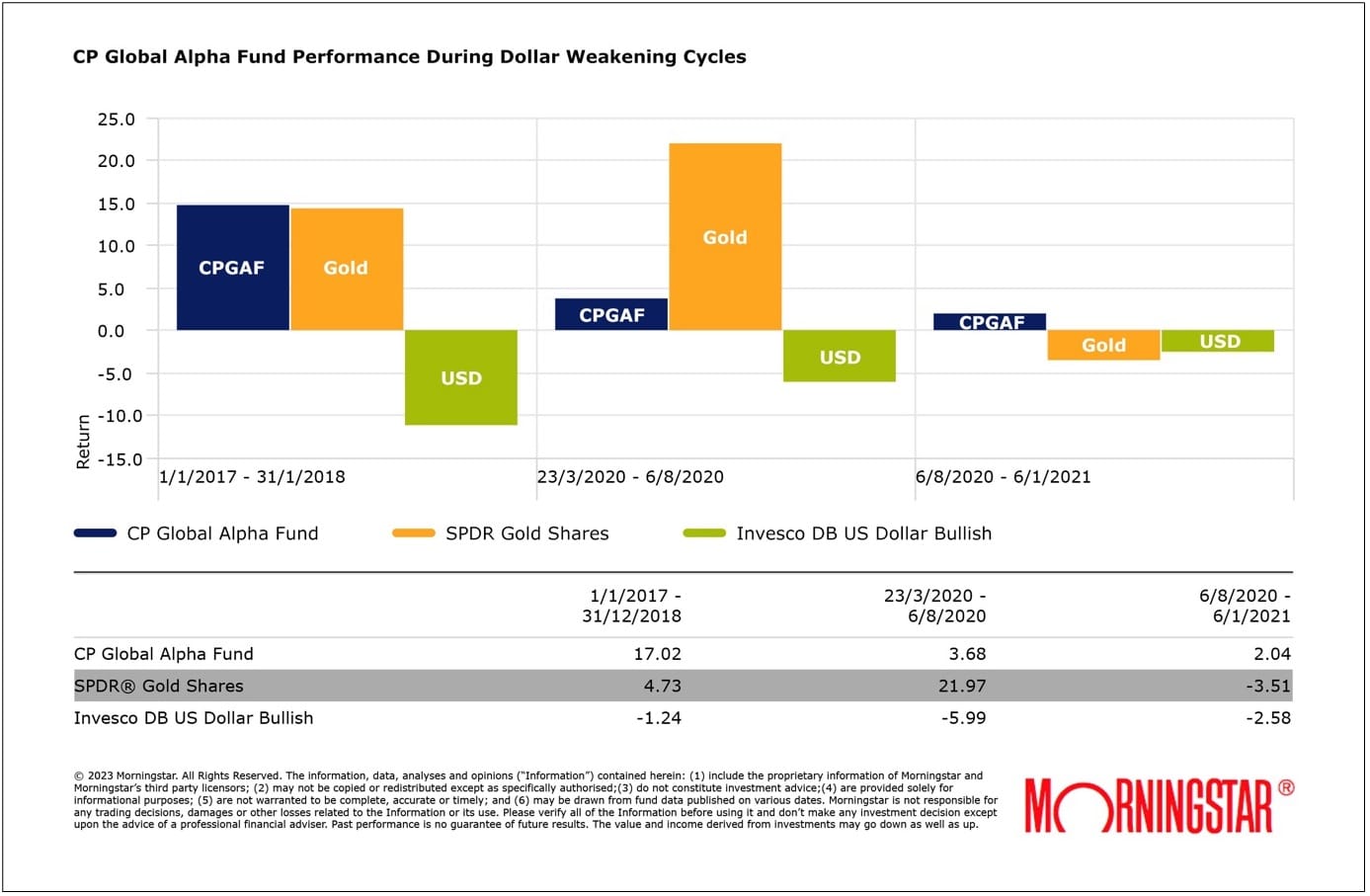

Chart 3: CP Fund Performance During Dollar Weakening Cycles

Based on Chart 3, CP funds have consistently performed well during phases of Dollar weakening since inception. This refutes the concern that CP fund performance would be negatively affected by a weak Dollar. Additionally, CP funds also employ hedging strategies as part of our global macro approach, thus offering investors the best of both worlds.

Q3. My concern is that a weakening Dollar will result in a lower redemption value when I convert it back to my local currency.

The conclusion that a weakening Dollar will "reduce" the redemption value is deceptive because it describes a quantitative measurement that depends on the point of measurement. The value may appear lower compared to the peak, but it could very well be higher if compared to your entry point.

For most of our investors who have a long-term investment target, they do not have such concerns as the performance of CP funds rebased in their local currency has shown a positive net appreciation over the years.

However, for investors who may be particularly focused on maximizing profits from currency exchange fluctuations and timing the peak, they should bear in mind that statistics have consistently shown that CP funds tend to achieve new peaks of NAV, rebased in the local currency, in the future. Chart 4 highlights the potential for investors to benefit from consistent, long-term growth by remaining invested, rather than speculating on currency fluctuations and redeeming prematurely to chase short-term gains.

Chart 4: Long-Term CP Fund Performance Rebased in Selected Local Currencies

Q4. What about investing in local or non-dollar-denominated currencies to eliminate the risks associated with the US Dollar?

Similar to the points discussed above, your decision to invest in local or non-dollar-denominated currencies should still take into consideration the expected potential value of the assets you are investing in, as well as exchange risk.

It is important to note that the majority of global investors, including professional investors, primarily invest in USD-denominated assets for two reasons: Liquidity, and the fact that the US Dollar is the settlement currency of the global financial system. When investing in smaller local capital markets such as Malaysia or Singapore, liquidity risk is a major concern. In addition, since financial trading contracts in global markets are mostly denominated in USD, investing through non-dollar-denominated funds may result in unfavourable exchange costs that erode your gains unnecessarily.

According to an estimate from the Bank for International Settlements (BIS), the US Dollar is involved in 88% of all global transactions, and when it comes to financial trading contracts, the majority are denominated in USD in terms of transaction size:

- Top-performing funds (99%)

- International funds (80%)

- FX market (85%)

- Commodities (80%)

- Global bonds (60%)

- More than 42% of global stocks listed in the US, with an estimated over 70% of global average transaction in the stock market being US stocks.

- Majority of futures and options contracts, ETFs, and other derivatives are also traded in USD.

Therefore, if you stay invested in major markets, you are likely engaged in USD-denominated assets. Most investment managers also price-in the Dollar value consideration in their strategies and portfolio allocations. More importantly, as a global macro hedge fund, currency factors are a primary consideration of CP funds; and naturally, its associated risks are actively managed on your behalf.

Q5. Can periodically withdrawing my investments help to mitigate exchange risk?

No, on the contrary, it goes against the golden rules of investing, which encourages dollar-cost averaging through ongoing reinvestment, and taking full advantage of long-term compounding effects to overcome inflation and maximise profits.

Investors who practice a 'draw-down averaging' approach, which involves periodically withdrawing capital from their investments under the assumption that it averages out their risk exposure, are doing more harm than good to themselves, as this ill-informed approach diminishes their capital gain as well as interrupts the compounding effect of their investments.

Interruptions to the compounding effect of an investment targeted at growth can have a significant impact on the final outcome, and in the context of CP funds, such interruptions can prove to be detrimental to the investor’s financial goals...

On this note, it is also important to highlight the misconception of comparing periodic draw-downs of investment from a growth fund vs yearly-dividends from a fixed-income fund. Due to the concept of risk premium, which is the additional return that an investor expects to receive above the risk-free rate of return in exchange for taking on additional risk, growth funds are completely different animals as compared to fixed-income funds which are by design – closer to the risk-free end of the spectrum.

In summary, periodically 'drawing-down' your investments in a growth fund to mitigate risk is an ill-informed approach to investing. Moreover, due to the fundamental differences in risk premium, investors should avoid making the mistake of 'drawing-down' their investments in a growth fund as if it was similar to drawing a dividend from a fixed-income fund.

Q6. What is CP’s view on the exchange risk of the US Dollar as of 2Q 2023?

Exchange rates are quoted in pairs, so it is necessary to consider the underlying factors of both currencies when defining exchange risk. Let us first look at the US Dollar…

De-dollarisation has gained significant attention this year, with calls to 'kill the Dollar completely' being echoed by anti-US groups across social media. However, when it comes to investment, a fundamental and logical analysis is necessary, as we have previously explained. While de-dollarization may be a long-term game, it could take decades before the King Dollar truly loses its crown. It is premature to predict the greenback's demise. There is nothing in the greenback’s recent performance to suggest that its status is in danger.

A number of separate political incidents have fuelled the discussion about de-dollarization, and the topic has become more prominent due to sanctions cutting off Russia from many dollar-based networks. Other nations, including Brazil, India, and Saudi Arabia, have made efforts towards de-dollarization, albeit mostly superficial ones, in the hopes of relying less on the dollar for their international exchanges. How far is the talk of de-dollarisation going to proceed? Probably not very.

A Long-Term Perspective of the US Dollar

Where will the Dollar move next?

Since peaking last September, the US Dollar has been on a downtrend, as investors anticipate that the high interest rates will have a negative impact on the economy while inflation continues to decrease. Investors are betting that the Federal Reserve will pivot from tightening to cutting rates in response. To predict where the Dollar will move next, we need to evaluate whether the forward-looking expectations on inflation and the Federal Reserve's policy, which have already been factored into the Dollar's current trend, will be realised.

Inflation

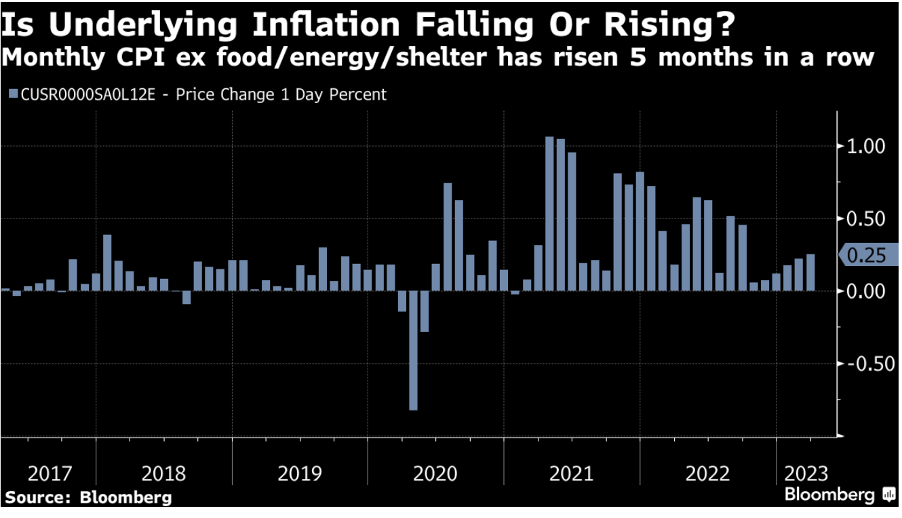

While there is evidence that inflationary pressure is easing, it still remains at a high level. We find ourselves at a particularly interesting stage in the inflation cycle as the monthly Consumer Price Index (CPI), excluding food, energy, and shelter, has shown a general decline since mid-2021, with each cyclical uptick resulting in a lower peak than the previous one in monthly underlying inflation. Despite this trend, this measure has seen an acceleration in inflation for the past five months. which raises questions about whether underlying inflation is actually falling or rising.

Federal Reserve Policy

Meanwhile, the labour market is starting to show signs of weakness, but it still remains relatively strong. The positive news is that the Fed's policies appear to be working, and a soft landing for the economy is still possible, which is beneficial for the Dollar. However, the downside for the stock market is that there is currently no immediate need for the Fed to change course, which means there is little reason to cut rates at this time. This suggests that the previous expectation of a Fed policy pivot towards rate cuts, resulting in a weakening trend for the Dollar, may be inaccurate, which could be supportive of the Dollar.

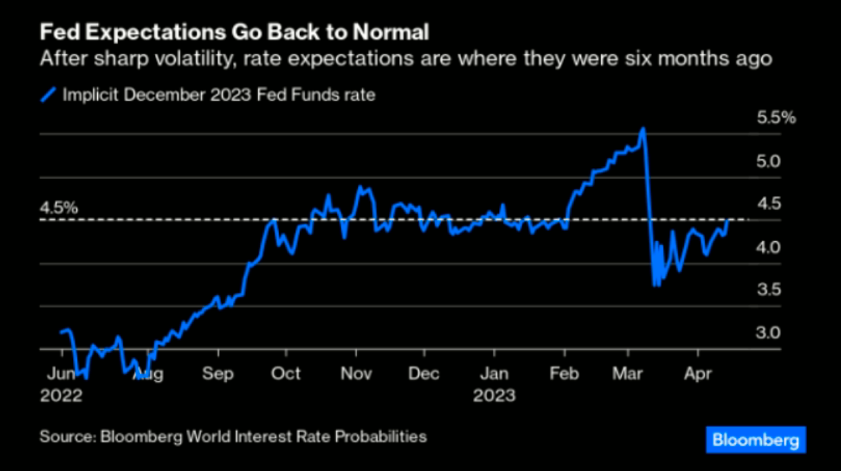

In February, robust employment figures were followed by a banking crisis in March, resulting in sharp fluctuations in US bond yields. As of now, future Fed fund rates are expected to be at 4.5%, which is the same as it was six months ago when talk of a Fed pivot was gaining traction and the Dollar began its weakening trend from its peak. The bond market is now indicating that the Dollar's near-term downside potential is limited, with investors finally revising higher their Fed rate bets for this year.

Market Positioning

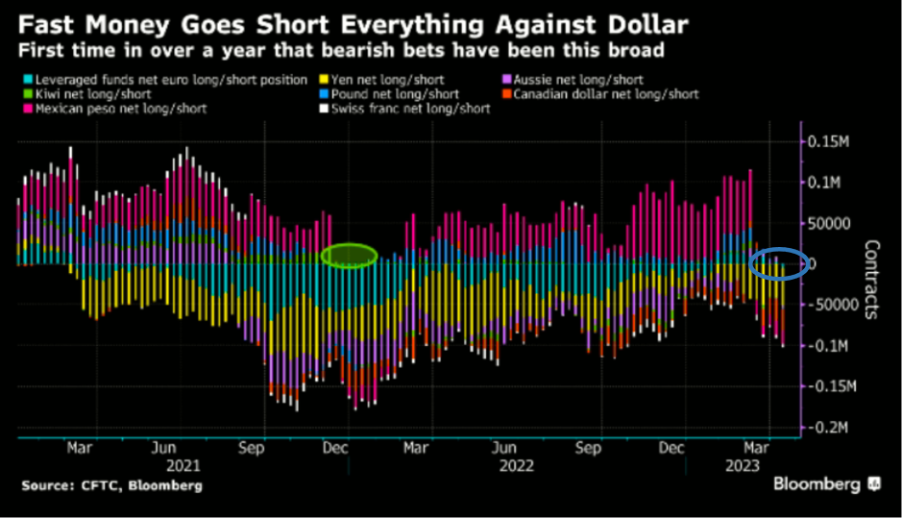

Investors' extreme pricing for Federal Reserve rate cuts has led to the greenback's longest stretch of weekly declines in almost three years. However, the latest data from the Commodity Futures Trading Commission indicates that this trend is about to reverse, as investors have now started to withdraw their expectations of a rate cut from the extreme level.

Leverage funds had a net short position on all major currencies against the Dollar last week (blue circle), marking the first time this has happened since January 2022 (green circle). A position below zero indicates a net short position, while a position above zero indicates a net buy position.

The last time leverage funds were net short on all major currencies against the Dollar (green circle), the Dollar began its rally from 95 to 115. Now that leverage fund holdings have turned net short again, it raises the question of whether the same rally will repeat itself.