2025 Annual Report

About CP Global Macro Strategy

Our investment approach focuses on executing trades spanning across a variety of asset classes, leveraging profit opportunities driven by our global macro perspective, unlike traditional asset allocation methods or conventional trading strategies. This low correlation to market approach enables us to respond dynamically to shifting narratives and capitalise on emerging trends, themes, and insights that arise from our ongoing analysis of global economic conditions, policy changes, and market sentiment.

We rely on a global macro lens to navigate and interpret changing market dynamics. The process begins with the top-down analysis of broad macro environments, evaluating macroeconomic trends, policy developments, geopolitical factors, global liquidity conditions, and systemic risk, amongst others. This broad view allows us to determine the prevailing market conditions, evaluate price levels for the respective asset classes and establish suitable trades by selecting the appropriate strategy(s) from our multi-strategy repertoire to address different market conditions.

This process ensures that our systemised investment approach and risk management framework are well-informed and data-driven, enabling us to navigate and capitalise on the opportunities to maintain stable growth across different market environments.

2024 Market and Investment Review

Navigating Opportunities and Risks in 2024

Our 2024 strategy anticipated that the strong stock market rally of 2023 would continue into the year ahead, driven by expectations of further Federal Reserve (“Fed”) easing and a 'Goldilocks' environment characterised by robust economic growth and corporate earnings. The core focus of our strategy aimed to capitalise on the sustained upward momentum of U.S. equities and employed a trend-following approach.

However, we remained vigilant, and were prepared to pivot toward contrarian or exit strategies if the rally showed signs of overextension or if significant risks emerged, such as a sudden economic slowdown, persistent inflationary pressures, geopolitical tensions in the Middle East, or economic headwinds in China.

We also identified the continuation of the rallying Gold trend that could serve as an ideal hedge against our bullish U.S. equities outlook, while offering an appealing alternative to the U.S. Dollar as a safe haven, particularly during a Fed easing cycle and in periods of heightened U.S. political risks during an election year. Rising U.S. deficits and increased central bank interest in accumulating Gold reserves reinforced its appeal. However, risks of hotter-than-expected inflation could exert downside pressure on both Gold and U.S. equities prices, demanding such a strategy to actively monitor the relevant economic data trends.

Meanwhile, the Yen carry trade remained a prominent component of our 2024 strategy, driven by wide yield differentials between Japan and the rest of the world. While this strategy presented compelling opportunities, we remained carefully prepared for potential risks of unwinding, including Yen intervention or increased rate hike expectations from the Bank of Japan (“BoJ”). The Yen carry trade strategy also anticipated that unwinding could trigger the selloff of high-yield asset classes, including U.S. equities and Gold, which were likely part of the carry trade targets.

Additionally, we maintained focus on event-driven strategies whenever appropriate, targeting opportunities arising from key economic data releases, government policy missteps and market mis-pricing, ensuring that our approach aligned with evolving market narratives.

Adapting to Shifting Market Conditions

The year began with persistent inflationary pressures in the U.S., as labor data and inflation readings exceeded prior expectations. This prompted markets to reassess whether prior optimism and positioning for Fed easing had outpaced the underlying fundamentals. Recognising a likely deviation from our initial outlook, we cautiously initiated shorter-duration contrarian trades, shorting U.S. equities and Gold, based on the expectation that hotter-than-anticipated inflation would exert downside pressure on these asset classes.

This strategy allowed us to navigate near-term mis-pricing while maintaining our conviction in the broader disinflationary trajectory we expected over the longer term. Our positions in Gold proved particularly advantageous, as they capitalised on the inflationary buildup and delivered strong returns.

However, our U.S. equities positions underperformed, as market sentiment shifted towards robust economic performance and positive earnings momentum, in a period where “good news” was unequivocally interpreted as such by market participants.

As inflationary pressures eased, early signs of disinflation reignited optimism around potential rate cuts. The Fed maintained a prudent stance and kept its rate outlook steady due to uneven progress on disinflation. This environment provided an opportunity to execute our contrarian strategy effectively in the U.S. equities markets, capitalizing on elevated valuations and the subsequent corrections in overextended rallies.

However, better-than-expected corporate earnings shifted the focus of market participants away from interest rate policy to broader economic performance more quickly than anticipated. This shift introduced volatility into our sentiment indicators, limiting further opportunities and leaving us vulnerable when the market unexpectedly shifted to interpreting “good news” as “bad news”. Despite these challenges, event-driven short positions in Gold, tied to U.S. data releases proved successful, reinforcing the adaptability of the strategy.

Geopolitical and Monetary Policy Dynamics

Geopolitical tensions added volatility to the first half of the year, particularly in the Middle East, where escalating conflicts, including Iran’s involvement, drove a flight-to-safety. The conditions allowed us to execute our trend-following strategy effectively, supported by the Gold rally which reinforced safe haven appeal during this period.

Once we assessed that the geopolitical conflict was largely posturing, we determined that the associated risk premium would fade quickly at these outstretched price levels, as indicated by our technical signals. In response to the shifted market conditions, we transitioned to a contrarian strategy by shorting Gold. These trades highlighted the value of a multi-strategy global macro approach, allowing us to effectively navigate transient risk premiums and adapt to evolving market narratives.

The shifting expectations surrounding a potential BoJ policy adjustment added complexity to market conditions, as sentiment oscillated between aggressive Yen selling by carry traders and Japanese policymakers issuing verbal warnings about Yen depreciation. While our initial outlook anticipated the persistence of carry trade trends, the market conditions began to steer away, as narrowing yield spreads between the U.S. and Japan signalled a potential sentiment shift. Improving economic data and hawkish rhetoric from Japanese policymakers further intensified speculation about a BoJ rate hike, adding to the uncertainty.

This shift in the balance of risks allowed us to take a careful detour to execute our contrarian strategy, focusing on short Dollar long Yen (short USDJPY) positions supported by oversold conditions and stretched valuations in USDJPY and the Nikkei index respectively. However, the market’s irrational Yen selling persisted, with technical factors dominating and overshadowing the narrative risks. Consequently, a handful of our Yen-focused trades during this period incurred losses.

The second half of 2024 marked a pivotal moment in monetary policy expectations as softening U.S. labor and inflation data reinforced expectations for Fed rate cuts.

By this time, persistent Yen selling had become disconnected from narrowing yield spreads, indicating complacency among carry traders and creating an ideal environment for Japanese policymakers to intervene in the FX market. The mis-priced market presented an opportunity to implement contrarian strategies by taking long positions in the Yen, supported by the high likelihood of interventions and oversold conditions.

After that, stronger-than-expected corporate earnings and resilient economic data reinforced the narrative of a soft landing, despite ongoing concerns on high valuations. Disinflation progress in a lower rates environment, coupled with robust earnings and the continued AI-driven growth story, provided fundamental support for U.S. equities. In this context, “good news” was interpreted as “good news”, enabling our sentiment indicators to generate clear signals for establishing momentum-driven long positions in the U.S. equities markets. This strategy was further bolstered by an attractive entry point created by the temporary pullback from the carry trade unwind.

Subsequently, the Fed enacted a jumbo rate cut while signaling a prudent, data-dependent approach to further easing, redirecting market focus to the pace and depth of the easing cycle, prompting investors to reassess their positioning. Simultaneously, the BoJ tempered expectations for further tightening and signalled no urgency for additional rate hikes.

This juxtaposition of policies across major central banks led to the continuation in Yen carry trades, as unwinding earlier in the year had run its course, resetting sentiment. Despite Japan’s gradual policy normalisation, its rates remained notably lower than those of the U.S. and Europe, underscoring persistently wide yield differentials. We successfully executed on carry trades, selling the Yen against the U.S. Dollar and British Pound through renewed opportunities provided by the clear divergent monetary policy outlook. Furthermore, political uncertainty in Japan – triggered by the Liberal Democratic Party’s (“LDP”) loss of a parliamentary majority which further weakened the Yen, enhanced conditions for our carry trade strategies.

As U.S. election uncertainty mounted, American equities remained subdued, though sentiment did not fully shift into a risk-off mode. Gold played a pivotal role during this period, serving as both a hedge against our U.S. equities positioning and a safe haven amid political uncertainty. Anticipating heightened pre-election hedging flows, we entered long positions in Gold ahead of the election, capitalising on the sustained upward momentum that drove the yellow metal higher. This occurred despite a strengthening U.S. Dollar and rising U.S. Treasury yields, which typically weigh on non-interest-bearing assets like Gold, suggesting a sentiment poised to reinforce its bullish momentum.

Following Trump’s victory, market sentiment experienced a shift as expectations of pro-growth policies fuelled sustained optimism in U.S. equities, reducing the need for hedging. We closed our successful Gold positions, which served as a hedge against our U.S. equities exposure, and pivoted to shorting Gold supported by overstretched price levels. This strategy allowed us to capture the subsequent downside in Gold as political risk premiums in Gold unwound drastically.

2024 was a challenging year for China, as weak economic recovery and persistent structural challenges weighed heavily on market sentiment. The economy struggled with a prolonged real estate slump, subdued consumer demand, and strained local government finances. Despite government stimulus efforts, growth remained under significant pressure.

Capitalising on Event-Driven Opportunities

Late in the year, policy development in Beijing triggered significant market volatility creating favourable conditions for event-driven strategies. In September, the announcement of new stimulus measures sparked a sharp turnaround in market sentiment, leading to a 20% rebound in Chinese equities ahead of the week-long holiday closure of Mainland exchanges. During this period, Hong Kong-listed China stocks, which continued trading on the Hong Kong exchange, drove the Hang Seng index to climb an additional 12%, driven by optimism around the stimulus package.

Recognising a mis-pricing opportunity, we initiated contrarian short positions on Hang Seng index futures underpinned by over-exuberant prices. This strategy proved effective, as the index corrected sharply following the reopening of Mainland markets.

Delivering Strong Results Through Strategic Flexibility

Concluding the year, our 2024 performance was defined by the ability to adapt to shifting market conditions while remaining aligned with our core strategies. Early in the year, persistent inflation led us to take detours and adopt contrarian trades, including short positions in both Gold and U.S. equities, to capitalise on mis-pricing opportunities. We transitioned back to momentum trades supported by disinflationary progress, leveraging corrections in the U.S. equities markets and achieving significant gains during the second half of the year.

Geopolitical tensions underscored the value of Gold as a hedge, and our active positioning allowed us to take advantage of opportunities arising from both its rallies and corrections. In the currency markets, our active management of Yen trades capitalised on key turning points, from early-year mis-pricing to mid-year interventions and the eventual resumption of carry trades. Through rigorous analysis of market shifts, disciplined execution and strategic flexibility across equities, Gold, and currencies, we successfully navigated the challenges and opportunities of 2024, delivering strong results for our investors.

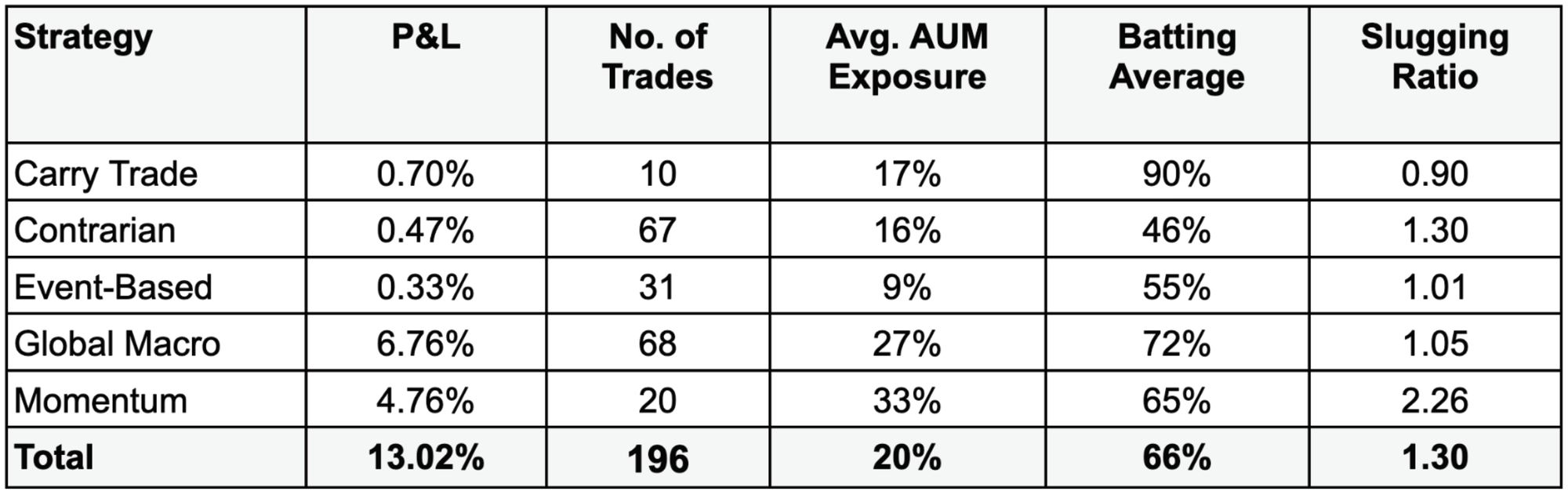

Trades Attribution by Strategy

2025 Outlook

Navigating Volatility: U.S. Equities and the Impact of Trump’s Policies

Our 2025 strategy anticipates a dynamic and volatile market environment, driven by uncertainties surrounding the Trump administration’s policy approach and its economic implications for growth and inflation expectations, further complicating the Fed’s easing trajectory. Ongoing trade tensions with China and other major trading partners, along with lingering geopolitical tension in the Middle East and Ukraine add to the complexities. We place particular focus on navigating the anticipated volatility in the U.S. equities markets, utilising Gold as both a hedge and a diversification tool, and leveraging opportunities in the Yen carry trade.

The core focus of our U.S. equities strategy remains to be cautious trend-following – the opportunities presented by robust earnings, advancements in AI, and expectations for tax cuts might provide some buying undertone in the first quarter, with later performance likely dominated by U.S. trade policy outcome. However, U.S. equities remain vulnerable to corrections, driven by the uncertainty of how market sentiment will respond to evolving narratives, whether leaning toward optimism around economic growth or concerns about inflation and policy easing.

Trump’s return to the presidency introduces significant uncertainty, as his policies present both opportunities and risks. Pro-growth measures like tax cuts and deregulation could boost corporate earnings, while protectionist actions such as tariffs and trade wars may drive inflation, increase business costs, and complicate monetary policy. This uncertainty, stemming from which policies will be implemented, their sequence, and economic impact, makes it difficult to accurately predict future developments. Elevated valuations in U.S. equities further heighten the risk of market instability. To navigate this dynamic environment, we will focus on event-driven strategies and shorter-term macro trades, maintaining flexibility to adapt as the economic and geopolitical landscape evolves.

Strategic Hedges: Gold and Yen Carry Trade in a Shifting Market

Following the long Gold trend is another core pillar of our strategy, serving as both a hedge against U.S. equities volatility and a safe haven during periods of heightened geopolitical tension and trade conflicts, exacerbated by Trump's hardline trade policies. Furthermore, rising U.S. deficits have encouraged central banks to accumulate Gold reserves, further supporting its appeal.

However, sticky inflation or stronger-than-expected resilience in the U.S. economy could challenge expectations of Fed easing, or a Trump-driven resolution with Israeli and Russian leaders could diminish geopolitical risk premiums – both putting pressure on Gold prices. These risks demand a disciplined approach – we closely monitor key economic data releases and geopolitical developments which may defy market expectations, to identify opportunities for contrarian or event-driven trades during any significant corrections in Gold, allowing us to both manage risk and diversify our portfolio effectively.

The Yen carry trade features prominently in our strategy, following the short Yen trend as supported by the backdrop of Japan’s domestic constraints. Despite periodic discussions about potential BoJ rate hikes which might introduce volatility to the market, Japan's structural issues such as aging population, stagnant wage growth, and subdued domestic consumption are likely to constrain the economy’s capacity to absorb elevated levels of borrowing costs. This allows the interest rate differentials between Japan and other economies, including the U.S. and emerging markets, to remain wide, sustaining carry trade opportunities.

However, crowded positioning and liquidity risks—highlighted by dislocations in 2024—require careful management. Any speculation about an enduring shift in BoJ policy or accelerated Fed easing could trigger unwinding scenarios, with potential spillover effects on high-yield assets, including Gold and the U.S. equities markets. In such events, we are prepared to pivot toward contrarian positions, such as shorting Gold or the U.S. equities markets, reflecting typical carry trade unwinding behaviours. By maintaining vigilance and monitoring policy signals, we aim to capitalise on both orderly and volatile market conditions.

Global Perspectives: European Growth, China’s Challenges, and Broader Market Opportunities

Additionally, we remain prepared to capitalise on event-driven strategies in broader markets whenever appropriate opportunities arise. European equities appear poised for growth, potentially benefiting from accelerated European Central Bank (“ECB”) rate cuts and a resolution to the war in Ukraine, which could significantly lift market sentiment. Meanwhile, China’s fragile recovery continues to be hampered by domestic structural challenges and trade tensions, demanding careful policy management to mitigate the risks of missteps.

Overall, our 2025 strategy centers around trend-following approaches, with the flexibility to pivot towards event-driven and contrarian trades in response to market disruptions.

Guided by a global macro lens, our strategies are informed by evolving market narratives and remain robust for the first quarter. Beyond that, Trump's policies and rhetoric are expected to significantly influence market behaviour, introducing uncertainties that would shape our longer term strategy, rendering year-long projections less meaningful now.

To address the fluid situation, we focus on actively managing risk exposure, monitoring key economic data releases, policy announcements, and geopolitical developments, aiming to deliver targeted, risk-adjusted returns for our investors.

To ensure our investors remain aligned with our perspectives, we will provide quarterly updates on our strategies and views. This report will articulate the rationale behind our trades, offering insights into the investment logic driving each decision. It will also present an assessment of current market developments and the considerations shaping our strategy for the next quarter.